Transcript: Economics of Ideas, Science, and Innovation Lecture 1

Dr. Benjamin Jones, Northwestern University

To read the launch essay and view the first video, visit this page.

To introduce this course:

I want first to discuss why we need a course specially about the economics of ideas.

We’ll talk about the nature of ideas, which is part of the answer to that question. Ideas are special and unusual goods that have very different properties from other kinds of goods.

I’m going to close by helping us think about spillovers and market failures.

This is an area where our free market welfare theorems tend to break down. That means that there’s going to be a distinctive role for policy in the innovation space — for particular institutions to try to overcome some of these market failures. In addition to innovation driving dynamics in the economy, this is also an area where there needs to be an enormous amount of policy. That gives you a whole different perspective, and there’s so much to be discovered still about what kinds of policies are effective.

Why a course on innovation?

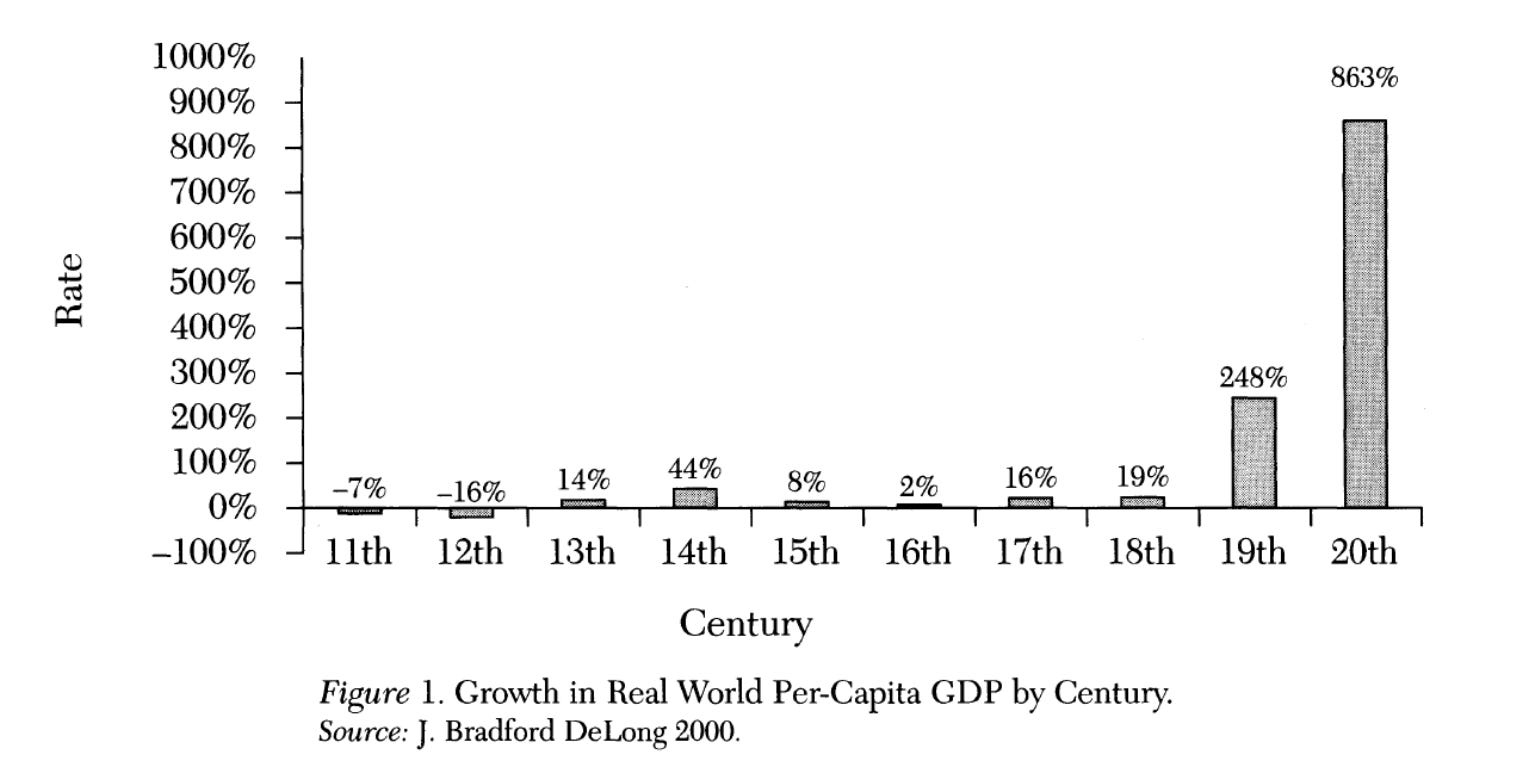

The advance of ideas is a profound, propulsive force for rising standards of living, increasing health, and longer lives. This is showing rates of increases in income per capita, in real terms, going back to the 11th century.

In the 19th and 20th centuries, we see a much more rapid expansion. This course begins with the Industrial Revolution. AI is the latest of a series of general purpose technologies that have been part of this explosive, ahistorical — from a prior perspective — expansion in standards of living.

You can try to get at why we think ideas matter here, and you could get into macro residuals. My colleague at Northwestern, Joel Mokyr, who just won the Nobel Prize this fall, has a book, Lever of Riches, which I read during my PhD and recommend to you strongly. It’s a beautiful, technology-by-technology take about how advancing ideas, often embodied in physical capital equipment, have greatly advanced productivity. It’s a very direct take on how important ideas have been throughout this period and particularly in the Industrial Revolution.

More powerful arguments for why we should think about ideas come from thinking about a particular sector of the economy and how it’s changed.

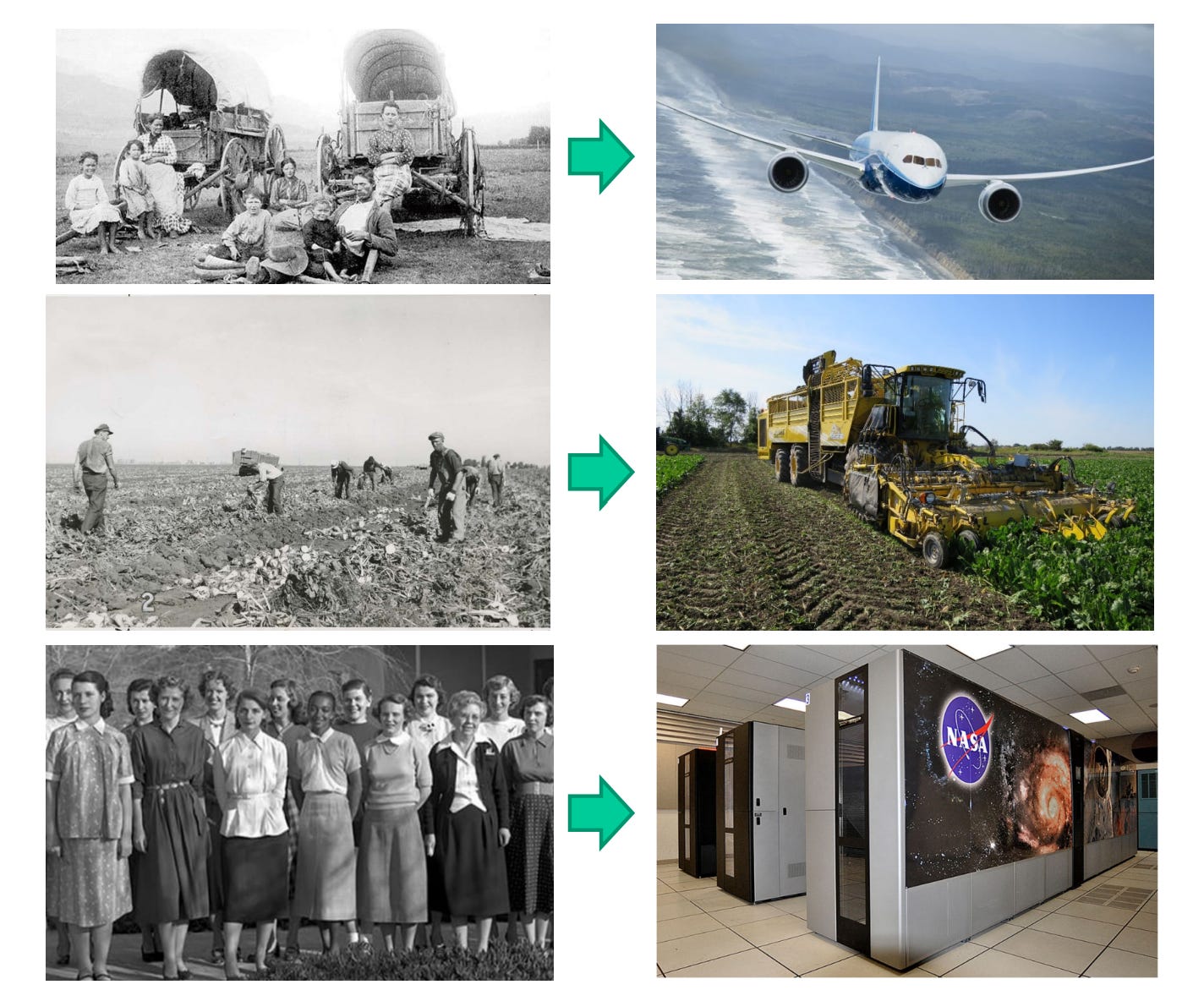

Transportation: In the middle of the 19th century — before trains, automobiles, and airplanes — if you wanted to get places, there was livestock; riding, or being pulled by, a horse. In the United States, if you wanted to go west you might be being pulled by oxen, who are going to be both your propulsion and possibly your food, because to get from Illinois, in the middle of the country, to California in the west, took something like six months. It was slow, dangerous, and you had to bring your own food. Today you can make that journey in less than six hours on a jet-powered airplane. Six months to six hours. How do we make that huge improvement in transportation efficiency? It has to do with a lot of new ideas that didn’t exist in the middle of the 19th century.

Farming: We used to do a lot of hand labor. Go back to the late 19th century in the United States: 80-90% of all people were farmers. Now it’s something like 2%. We’ve had incredible improvements in productivity including mechanized agriculture: machines that can sow, harvest, and process grains.

Computers: If you’ve seen the movie Hidden Figures, it’s about a team of women at NASA who were, as a job, called “computers,” because that’s what they did. They would be computing, by hand and with slide rules, orbital trajectories for launching satellites. They were replaced by what we think of today as computers, which are machines. At first they were replaced by an IBM mainframe. We know how much the advance of computing has done in terms of the breadth of effects across society.

We didn’t get to our standard of living today by saving and doing more of what we knew how to do in the 19th century. We’re not richer because we have more wagons per person. There’s something very different going on — we’re coming up with better ways to transport, harvest, and compute. Those are driving massive increases in output per hour, and advancing standards of living.

In those pictures we’re not seeing the ideas — we’re seeing implementations of those ideas: machines, for example.

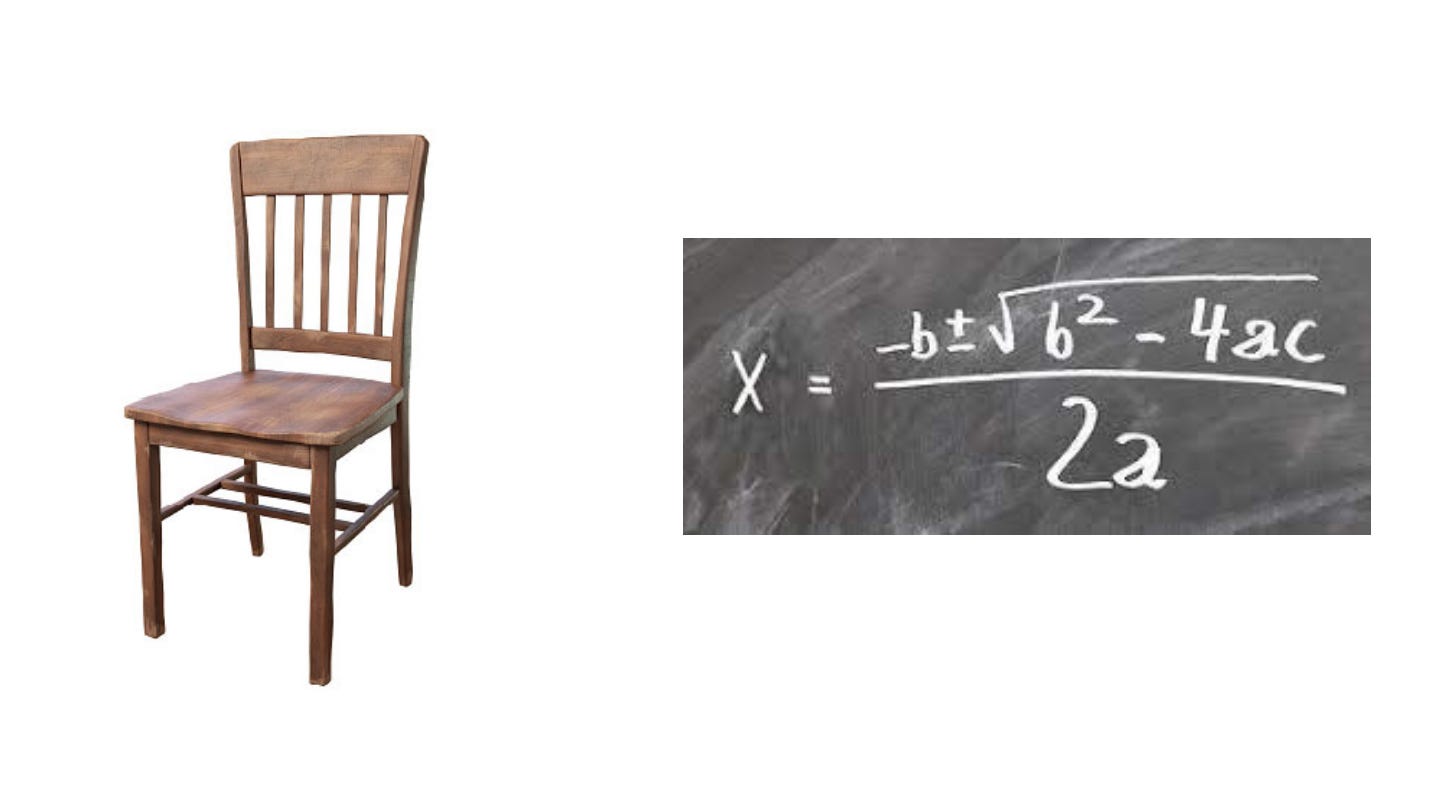

Much of economics is built around the thing on the left — chairs. We think about production functions, prices, markets, and firms. But the thing we’re talking about in this course is on the right: it’s an idea. It’s the quadratic formula. One way to encapsulate that distinction is that there’s a knowledge production function that might be quite different from a production function for ordinary goods or services, like chairs.

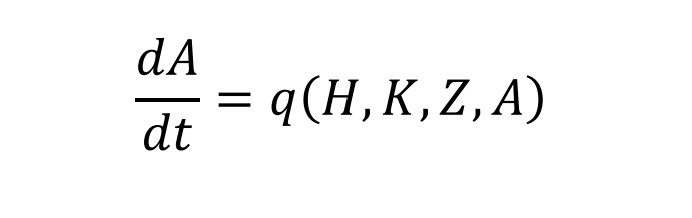

To put it in formal terms, pretty much everything you’ll hear over the next 13 weeks is going to fit into this equation.

What is the output on the left-hand side? A is some stock of knowledge, or maybe a measure of productivity or health, like how long you live, or survivability from a disease. We’re trying to improve A over time. The output of ideas is an improvement in the standard of living, through increases in productivity or health.

On the right-hand side, in that function q, I have the natural inputs.

H is human capital. There’s a lot of human capital going into ideas production, which might be distinctive from the human capital that goes into ordinary production of a chair.

K is physical capital, like machinery, where you’re going to use a lot of specialized machinery like telescopes, or microscopes, or particle accelerators, or a lot of Stata or R doing statistics in economics.

Z would be the institutions that are going to shape incentives: rewards for creating ideas, which are very distinctive in science and R&D from other institutions in society.

Then there’s the current state of knowledge itself, A, which may have an implication for the ease with which we can continue to improve our understanding.

I’m not going to talk about AI today because I’m doing an introduction. But if you want to think about AI, AI is K — physical capital. A necessary input into idea production through history has been human minds — without that, you can’t make any progress. You can think about AI as shifting some of that to K. Maybe it’s really high quality K. To be determined. But that’s one way to think about AI in a coherent framework.

Thinking about supporting innovative activity, a wide range of institutions and policies are directed at this peculiar activity of idea production. You’ve got:

The US Patent and Trademark Office: the patent system supporting private incentives to invest in research and development.

Grant funders for science like the National Institutes of Health, or the European Research Council.

Laboratories where things are actually happening: multinational collaborations like CERN for particle accelerators.

On the bottom, that’s my university. I’m sitting along that lake right now. Lots of labs here doing things.

Argonne is not a university but a US national energy laboratory.

The Howard Hughes Medical Institute is a philanthropic, very high-end health research lab.

Government funders for more solution-oriented process like DARPA, which is within the US Department of Defense, trying to come up with defense solutions to various problems.

Venture capital funders like Bessemer.

Philanthropies like Sloan.

Private sector corporate labs like Abbott, which is trying to come up with new drugs for medical devices.

There’s a wide range of private, nonprofit and public institutions coming up with new ideas, funding them, or coloring the incentives with which we do things.

To encapsulate the first question for our course, why have an economics of ideas? First, because the advance of ideas informs central phenomena. It’s an incredibly powerful, first order force in understanding the path of economic prosperity, which would include income, health, and also how inequality evolves between labor and capital, and between different kinds of labor. It’s about the dynamics of how markets, industries, and international trade work. It’s about the role of specific institutions and policy that are suited and designed particularly for this peculiar space of idea production.

We talked about the chair versus the quadratic formula — there’s something about ideas that’s distinctive, and I’m going to try to clarify that in an introductory way today. It’s from those distinctive features that you can begin to build out this more complicated, rich understanding of idea production and all of its features. The related issue, which I’ll come to very quickly now, is that because of these special features of ideas, it’s natural to think there are very large market failures. The market is not going to produce ideas correctly, left to its own devices, and that’s why we need public policy and places like Institute for Progress to help think about how we can do that policy better.

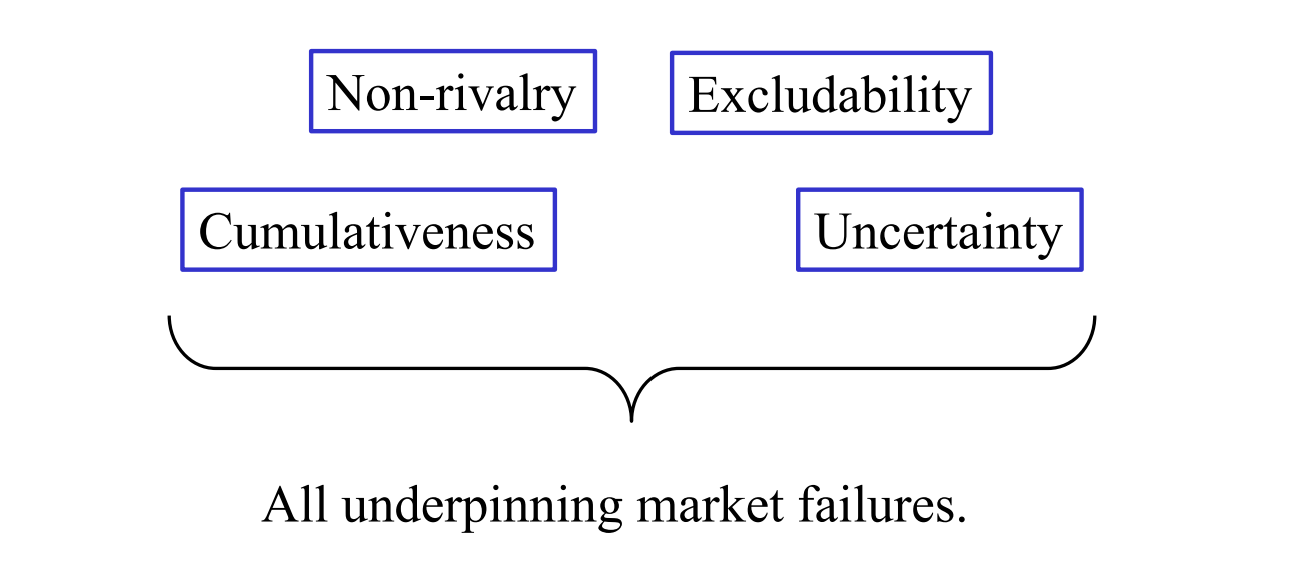

I want to talk about the nature of ideas, and I’m going to come to several features: non-rivalry, excludability and cumulativeness. I’m not going to talk much about uncertainty in the interest of time, but I can mention it. These are features that are going to underpin the market failures associated with ideas, and in some sense this course.

Non-rivalry

This is a somewhat odd concept when you first hear it, and then it becomes very natural. Most goods are rival goods: chairs, cars, or computers. If you’re sitting in the chair, no one else can use the chair at the same time. You’re rivals. If someone is driving a car, you can’t be driving that same car somewhere else at the same time. If you’re getting a visit with a dentist, they can’t provide that service to somebody else’s teeth at the same moment. Ordinary goods and services are rival: if one person’s getting the service or using the good, nobody else can at the same time.

But with ideas, at the core of it all is this concept — like the quadratic formula. Let’s say I’m using the quadratic formula right now to solve some algebra problem. Andrew could be using it at the same time. So could Matt. So could all of you. There’s no sense in which my using the quadratic formula is at all influencing your ability to use and get value out of it. We’re not rivals. If I’m driving the car, you can’t drive the car. But if I’m using the quadratic formula — no effect on your ability to use it.

Ideas have this non-rival property: algebra, a biomedical concept like the germ theory of disease, the use of an assembly line. Once Henry Ford puts in an assembly line to make cars, every other car company’s like, “Maybe I could do that.” Or you’re making something else, scaffolds, or chairs — I could use an assembly line. A chemical process. Regression: if I run Ordinary Least Squares, you can too. Jennifer Doudna comes up with CRISPR. Now that might be patented and be a source of some debate, but when the patent expires, people can use it for free. There’s nothing fundamental about the idea that would say that your use of CRISPR would make it harder for me to use it.

That property, which is essential, is going to have very important implications. It’s going to mean that there’s a lot of value in ideas because value spills over. If one person creates it, it can spill over to other people. That’s going to lead to market failures. This course is going to suggest that markets are going to underinvest in new ideas. If the markets underinvest, we’re not getting enough of this incredibly important thing. So we’re going to want to care a lot about policy.

If it’s non-rival, let’s say one of you comes up with an idea, and you put it out in a paper and everyone’s like, “Wow, it’s a new method,” or insight, or fact. Other people will be like, “I’m going to start making use of that.” But because everyone else is getting value from it, that means that you, in creating it, are not getting the whole value of it to society. You’re getting the value you use it for yourself, and then its value is spilling over through non-rivalry to all these other people. So there are positive spillovers.

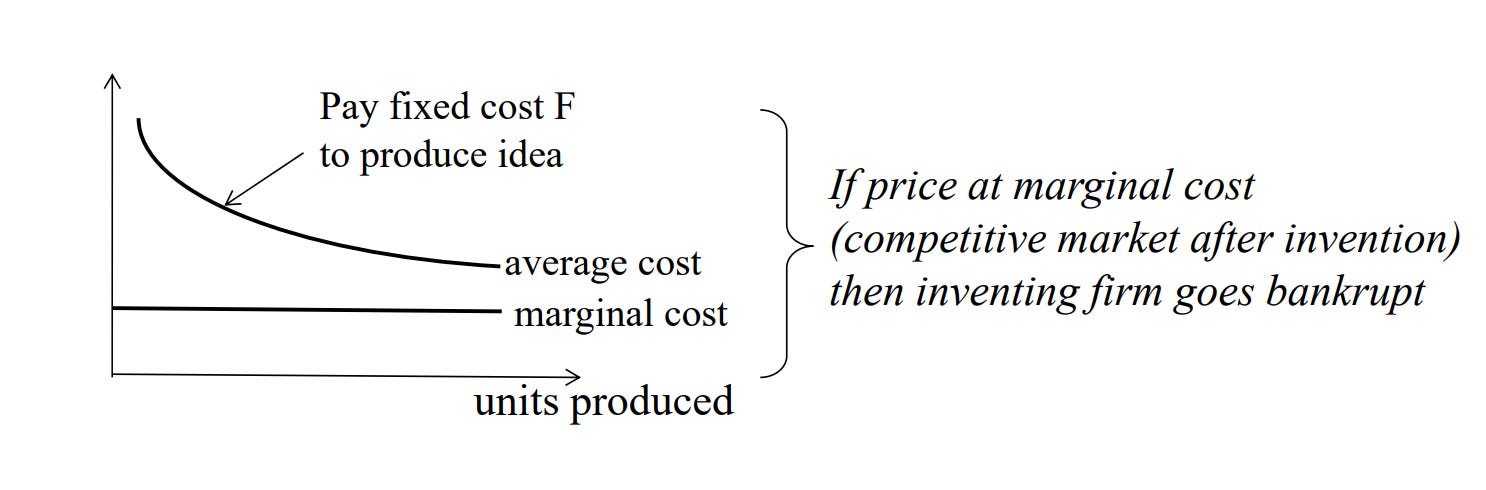

But where it becomes more problematic from a market investment point of view is as follows. The first time you come up with the idea — let’s say you’re going to write a book, or record a music album, or come up with a new pharmaceutical that fights a certain kind of cancer. Often the act of creation, like writing a book, is quite expensive. It takes a lot of time and effort. Coming up with a new pharmaceutical can cost a firm hundreds of millions of dollars to find it, show that it works, and that it doesn’t have bad side effects. So there’s this huge fixed cost to producing an idea. But if you show the pharmaceutical works, other people — if they could access the pharmaceutical — could make copies of the pill, not having to bear any of that fixed cost. If you make a book and everyone could make a copy and read it as a PDF. If you recorded an album at some expense and then everyone else can listen to the music and make copies and we all can listen to the same song at the same time for free. It’s non-rival. Then what happens? A market’s going to make it hard for this work.

Why? Here I’m showing you the units of ideas produced along the x-axis. But there was a fixed cost to come up with the idea. For the person who created the idea — they’ve got this fixed cost of coming up with a pharmaceutical and they’re going to make more copies of the pill, so their average costs are going to decline. But because of the fixed cost, their average cost is always going to be above the marginal cost of making a pill, because they still have to pay off this fixed cost of producing the drug in the first place.

Any entrant who wants to make copies of the pharmaceutical, or the song, doesn’t have to pay that fixed cost — they just make copies. Which means that if competitive entry happens, they’ll come in, and they can price just above their marginal cost and make money, but they’re going to be pricing below the average cost from the idea creator. Who’s going to win the market? Not the idea creator. They can’t charge that low because they have to pay themselves off for the fixed cost of creation. It’s the entrants who come in and copy with the non-rival ideas that can serve the market at the lowest price. So the person who actually did the invention goes out of business, from non-rivalry alone, if you let that be the dominating force.

In a context of non-rivalry, it’s very hard to invent. You might do it because we’re creative. I like to write a book; it makes me feel good. But you’re probably not going to marshal hundreds of millions of dollars to make a drug, because you’re going to lose all your money even if you’re successful. This is the first key market failure, and we need to solve it. To solve it, we have to get to a second concept, closely related to non-rivalry, but it’s more of a choice of society, which is excludability.

Excludability

Ideas themselves are not typically naturally excludable. They’re non-rival. If I heard about the quadratic formula, I’ll just use it. If I’m going to come in and use it for free — and I might undercut you who created the idea — in order to create a private decentralized incentive for someone to create that idea, we need to let them exclude others from using it. In other words, we need to give you something like a patent. If you did a pharmaceutical, and I could come in and undercut you and there was nothing you could do about it, you would have no incentive to invest. But if I give you a patent, I make you a monopolist — that gives you the right to exclude others from using your pharmaceutical unless you want to let them. You could charge a license or a royalty to let them do that. If it’s my pharmaceutical and I have a patent, I can decide who gets to produce it. Now I can charge a much higher price, and then pay off my fixed cost of investment. That’s a legal solution relying on creating intellectual property.

In general, whether you have excludability is going to depend on things like the policy institutional space in a country and the strength of the legal system. It can also depend on the technology itself. The patent system is the most obvious form of creating excludability. Think of it like this. Ideas are non-rival. But you can choose to make them excludable by allowing patents. Other intellectual property would be copyrights, trademarks, non-compete agreements, or trade secrets. There are other ways to do it which cover different kinds of creations. It’s up to a society to decide how much legal protection we want to give to certain ideas and creations, how long the patent right should be, how long you want a monopoly around these design questions.

The other way to go is not necessarily relying on intellectual property. A company or a person might get excludability in other ways. One thing is you can make it really hard to copy. The idea itself is non-rival, but you might encrypt it. An example would be satellite radio. If you’re driving around, the satellites are sending down the radio signals to all cars. Everyone is getting the signal, but you can’t listen to it unless you pay a subscription, because that is going to give your decoder in your car the decryption ability to listen to that channel. So there we don’t need patents. You could play a video game online peer-to-peer on some server and they don’t have to have a patent or intellectual property — because they can control your access to the server, and you can only play the game if you have access to the server. If you can control some necessary gatekeeping thing, or keep it secret, and people can’t figure out because it’s an internal process to your firm, maybe you can get excludability, despite the non-rival nature of things. This is why we’re going to have things like the patent system, because we need to create some incentive where the market without that property right would not succeed.

Uncertainty

Uncertainty is an absolutely fundamental feature of ideas. It’s not just that I’m going to flip a coin: is it heads or tails? I’m not sure. There’s that element where you’re not sure. If you start a drug program, 9 out of 10 pharmaceuticals that go into the first phase trial don’t make it through. They think they might work, but until they try it — they’re going to fail most of the time. Venture capital firms — 9 out of 10 bets are losers. They’re going to lose most of the time, and hope that some bets are really successful and on average carry the portfolio.

But it’s not just that you have a 1 in 10 chance. It seems to be that we can’t even foresee the reason an idea will be valuable or not. Before the internet, there’s NSFNET; before that, ARPANET. ARPANET was created by DARPA, a research agency in the Department of Defense. What were they doing? Let’s say we’re trying to communicate with each other across our operations, but someone knocks out one of our communications towers. We want to have a robust system of communication so we can still communicate. The idea was that you would divide information up into packets, and send it on many different routes through a network. If you lose one node of communications, information can still be rerouted across different nodes and people can still be in communication. The early idea of the internet for them was robust communications when you’re under attack. Were they thinking about Amazon, Uber, or e-tail? They were thinking none of those things. ARPANET was around for a while before anyone began to think, “Maybe this could be useful for something else.” So it’s very hard to know which ideas are going to take off.

Cumulativeness

The other feature of ideas that’s very important is cumulativeness. You create a spillover. It’s non-rival. If I come up with a song, other people can listen to it. If you read a book, other people can read it. But it’s not just that they can imitate or use the idea. It’s that that idea has an influence on future idea creation. Sometimes math achievements look like, “What’s the use of that?” But then later they prove important because they unleash further applications. An advance in physics might lead eventually to a new material, and that changes how we design airframes. So there’s an intertemporal spillover. Another version is you create a smartphone platform. Having created that, people can write apps for it. So there’s an intertemporal spillover on the ability to do software applications.

This intertemporal part seems very fundamental to knowledge. The most quoted line in all of innovation studies goes back to Isaac Newton, who said, “If I have seen further it is by standing on ye shoulders of giants.” He wrote this in a letter to a contemporary of his, a physicist, Hooke. He’s saying, “I can take a step forward because I have the benefit of all the knowledge that’s already been accumulated, from which I can step forward.”

If knowledge is cumulative, if there’s much more that is known now and that’s an input into future knowledge creation, does that make your lives as young economists easier or harder? Does it make it easier to do research today and come up with a big idea?

In one sense, there’s a lot more known and a lot of those things are tools. We can search the internet, look at Google Scholar, and read lots of papers. AI is a new tool. If you want to do econometric analysis, it’s easier doing it with modern computers than with punch cards on a mainframe, or before that trying to do it by hand, writing down the matrices and inverting them — that’s a pain. So certain tools make it more productive. Also the constituent matter that we can build on is vast; so we have lots of opportunities to combine things that are new.

On the other hand, and the thing I’m going to go in the direction of, there’s so much more known, so it’s harder to get to the frontier, because you have to learn something of what’s come before. Every year, there’s more that has been discovered. In some sense that’s an accumulating mass of knowledge. That’s what I call the “burden of knowledge,” which has the effect of making people narrower.

This is one of my earlier ideas in research. I hope the burden of knowledge is an evocative way to think about it. The question is, what happens if there is an advancing stock of knowledge, from the perspective of human capital accumulation and ultimately innovative potential? We’re born knowing nothing. You haven’t been taught anything. You know certain things instinctively and then you have to go learn. But you’re being born, with every passing year, into a place with so much more knowledge — biological, statistical, mathematical, knowledge of the known universe. How can you respond to that? You’re born knowing nothing and there’s a bigger mountain of knowledge that you’re confronting.

You have two options:

You could spend longer in school, spend more time training, as there’s more to know.

You could say, “I can’t possibly know everything, so I’ll become much narrower.” Maybe going back in Plato’s time, the inspiration may have been the same, and Aristotle could make all these contributions across the waterfront of knowledge at the time. But you can’t really be a leading biologist even anymore. Biology is so many sub-areas. A physicist, meaning what? You do cosmology, or quantum, or solid state physics and materials. These are very different math, and sets of ideas. So people get much narrower.

It may be that computers are making us more productive, and there’s lots of great ideas and they make us more creative and inspiration is quite the same in terms of a process. Yet if we spend more of our life cycle training, we have less time, other things equal, to innovate. We see this in the data. A bachelor’s degree used to be the ultimate degree in electrical engineering. Then back in the early 20th century there’s a master’s degree, then a PhD, now they do postdocs, so you spend much longer in your early years training.

More importantly, we’re narrower. If you’re narrower, that means the constituent matter that you can be inspired from is quite narrow. You’re doing some combinatoric search, based on things that you know — that are within your specialty. But also, your ideas are probably applicable to your specialty, and may not be as broad in their impact, because you yourself are narrow. So maybe we’re all branching into these niches. Our ideas are important in those niches, but there’s so many niches, and your collective impact — on productivity as a whole and on the economy as an individual researcher — is low.

You’re going to hear from Chad next week about idea-based models for economic growth. One of his main findings, early in his career, is that we seem to be putting a lot more effort into R&D — more people, more money — and getting less out in terms of Total Factor Productivity growth per person or per dollar spent. You could think of this narrowness effect of the burden of knowledge as one way to explain that phenomenon.

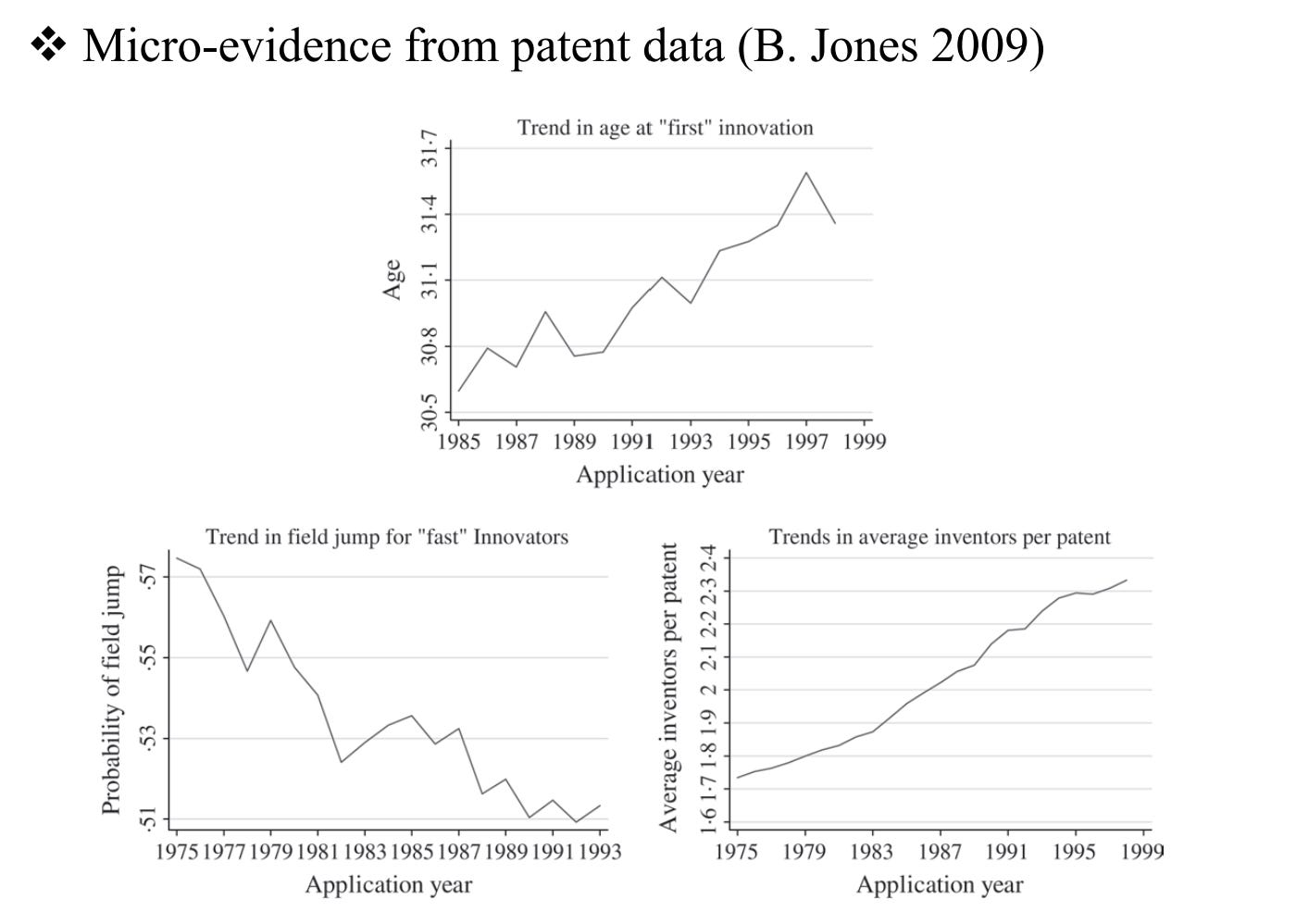

I had that idea when I was getting my PhD, and I went out using patent data — which is what we had — and looked at various patterns.

This upper picture is the age at which people get their first patent, and it looks like that’s going up. Another version of this in another paper is the age at which people do Nobel Prize winning work — not when they win the Nobel Prize, but when they do the research for which they would win it. Or people who are known technological inventors, like Thomas Edison and the light bulb, or Bell with the telephone — how old are they when they produce these signature contributions? You can see that the age at which people make those contributions is going up. If you unpack all this, you’re going to find that it’s going down in your 20s. You can still produce Nobel Prize-winning insights in your 20s. It’s just much less common now than it used to be, and people are typically peaking in their early 40s.

If you look at the lower rows, the one on the left is a measure of narrowness. It’s looking at an inventor and saying, let’s get two patents in a row that they do and ask if they’re likely to jump between one technology class on the patent to a new technology class. They’re less likely to jump with time, suggesting people’s ambit of research is more narrow.

On the right is one of our classic responses, which is — if everyone’s getting super narrow, what we might do is work in teams to pull together complementary forms of expertise. You see that too across all forms of patenting and science. Not only that, you see that teams are increasingly the source of the higher impact work. It used to be, in fields like math, if you wrote alone, you would do better than if you worked with a co-author or in a team. But now we see that reverse. Even in math today you’re going to have higher impact work if you work in a team than if you’re working alone.

Maybe AI is going to make you guys very productive. On the other hand, there is this training niche challenge that you have to overcome, and our classic solution to that is collaboration. Something you want to be thinking about, if you’re really good at econometrics but you aren’t a theorist, or vice versa, rather than bite your head against the wall of the other thing, can you collaborate with someone who brings those complementary skills together with you and produce a stronger paper more quickly.

Spillovers

The last piece I wanted to talk about was spillovers, to start bringing us around to the idea that this may be an incredibly high return activity and that we may greatly underinvest in it. That’s going to open up the policy and institutional space to us.

I had two papers I was going to talk about. One was Bloom, Schankerman, and Van Reenen, which asks whether firms’ R&D spills over to other firms, and what the returns are. A firm investing its own money in R&D is trying to come up with better products or services, or lower cost production methods, and they would capture the value of that themselves. But to the extent that they’re putting in place new discoveries, products, or services, other firms could learn about that and then be inspired for spillovers to do it themselves. That would not go to the private return of the firm. In fact, it might go against the private return of the firm because the other firms would now compete with them with imitative ideas. So this paper tries to pull apart key dimensions in those spillovers in a very clever and successful way. Given the time I’m going to go to the second paper, also because you’re going to hear from John Van Reenen directly later in the quarter.

Let me ask you a different question about spillovers. There are a number of spillovers in ideas:

There’s non-rivalry. You produce some new idea and get some value out of it, but then I see it. I can use the idea if it’s not excluded through a patent, and then I get value out of it. Even if it was excluded through a patent, I could probably be inspired by your thing and come up with my own version, which doesn’t quite violate your patent, but still you inspired me and I got some of the value. That’s what we call an “imitative spillover.”

There’s the intertemporal component. By producing a new mathematical idea, the next person can say, “That inspires me to something else,” and they’re going to capture the value in some intertemporal sense.

If you make something new and you sell it in a market, people are willing to pay for it. They’re paying because they’re getting value in excess of what they’re paying. The consumer of your ideas is getting a consumer surplus benefit from your creation that is not going to be captured by the creator.

So there are several reasons to think that idea production would be undervalued. The private inventor, or the scientist, is getting less value personally than the social value that is created.

On the other hand, there are a couple of forces that might go the other way. One feature among private sector players is what we call business stealing. Let’s take Amazon. They’re going to come up with a new business model based on buying and selling things online and delivering them to you — originally books. They’re going to kill a lot of existing brick and mortar bookstores that find they’re not able to compete with Amazon. There’s going to be a huge shrinkage in the bookstore sector. If you think about the private returns to Amazon, they’re doing something that is valued by consumers and there’s some social gain. On the other hand, the private return of Amazon is also a transfer from the existing bookstores to Amazon selling them instead. That isn’t a social gain. It’s just a transfer. They are stealing business from the existing bookstores. That could mean that the return to the investors in Amazon is too high, because a lot of what they’re getting is stealing other people’s business but not really adding much that’s more efficient to society. So business stealing can be a negative spillover of innovation. It’s part of the creative destruction idea that you’d see in Philippe Aghion‘s work, who also won the Nobel in the fall, working with Peter Howitt.

Then the last one might be a racing phenomenon. If we’re all different research teams spending money and time in a race after a superconducting material, or a particular new drug, it’s like a tournament. One of us gets the patent, or the discovery, then the effort of all the other teams may be partly or fully wasted. In racing for certain opportunities, we may overinvest because we have a congestion or crowding externality on each other, or duplication externality from the perspective of the research spend.

In reality, there’s stories for positive and negative spillovers. It’s very much an empirical question, and papers like Bloom, Schankerman, and Van Reenen looking at business behavior net it out among the businesses in the sector and say, “It looks like on net a very positive spillover.” But even that is quite limited. What firms are doing is not really science. What about science like math or physics, and what about all that’s going on in universities? That’s a trickier question, because for a lot of things the spillovers are very diffuse.

Here are three examples.

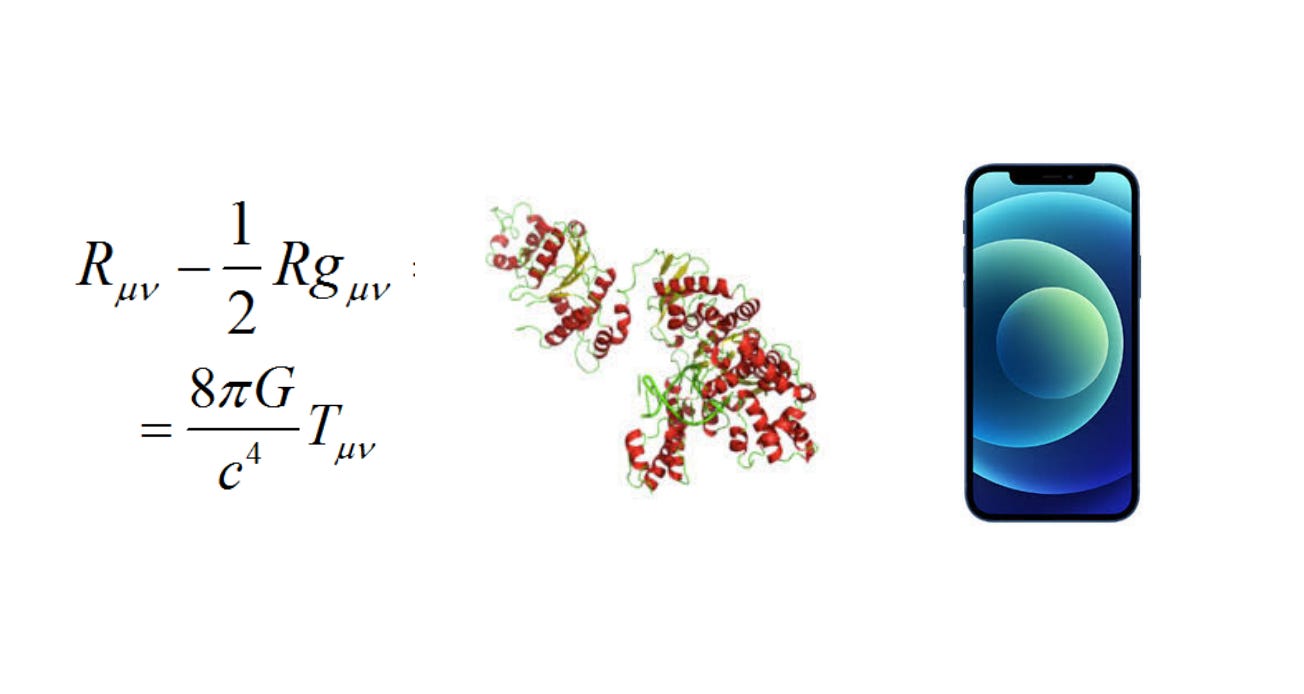

On the left, that equation is general relativity — that’s Einstein in 1915 and 1917. You might say, what is the benefit of general relativity? It’s a curiosity about the curvature of spacetime, and you might think it’s intriguing and neat, but not really useful. But it turns out that it’s incredibly useful. GPS satellites all work on atomic clocks that are very accurate. Those clocks have to be adjusted according to that equation, because they’re at lower gravity up in the air, and they’re moving at a speed compared to the surface of the earth. It turns out that if you don’t correct for general and special relativity, the whole GPS system doesn’t work. So you don’t get Uber — where we use GPS for drivers to find you and to navigate — unless you have the GPS system. You don’t have the GPS system unless you have relativity. That’s a hundred-year delay.

That equation is an application of Riemannian geometry from the 1860s I think. Riemann came up with a geometry in math that seemed like it had no application. He was wondering about the geometry of spaces in more than three dimensions which have curvature. This non-Euclidean curving geometry in high dimensionality seems completely useless, because we live in three dimensions, and things aren’t curved. We can do everything in orthogonal planes or whatever. But it turned out that when it got to time and space there was a fourth dimension, and it turned out that mass was curving them, so the appropriate mathematics 60-70 years later for Einstein was Riemann. That’s going to lead to GPS. In other words, if I were to ask you the question, what’s the social value of geometry or general relativity, it’s a hard question to think about because of these really long lags. Obviously you need it. It’s necessary, but it’s not the only thing that’s necessary to the GPS system or Uber. So how would I allocate what the value of all that mobile internet I could put back on these equations? It’s very hard to think about.

The one in the middle is Taq polymerase. That’s a protein that is the heart of Polymerase Chain Reaction, which is the heart of all modern biotech. It allows you to make millions of copies of the same strand of DNA, which we use for any kind of genetic engineering, or forensics, or PCR, as you probably know from COVID tests. That protein was discovered by a couple of biologists in a hot spring in Yellowstone. The organism it’s in is a bacteria that lives in really high temperatures, and at the time it was just a biological curiosity. That was in the 1960s. It turned out that that is going to unleash, a decade or two later, the entire biotech industry, and without that protein you can’t do it. What’s the social value of that research? This is now stuff that’s being funded by a government science agency.

I put the iPhone up there because — try to imagine enumerating the social value, or cost, of the smartphone. It’s complicated, because there’s so many things it touches. How would I begin to think about these spillovers and all these different margins from that one device? So it’s very hard to do social returns in some adequate way. The more important the technology, the wider its use, probably the harder it is to measure, and we don’t want to miss those.

I want to close with one idea on this. There’s a big literature on how to calculate the social returns to R&D or to science. I’m going to give you a conceptual take that’s more macro, which I think will help motivate why what we’re doing in this course is so important and why we need policies. If we believe ideas are central to advancing prosperity — which I think there’s a huge literature coming from many angles telling us — without which we don’t really grow among advanced economies over the long run, could we harness that insight to think about the social returns from a macro perspective?

This goes to a paper I did a few years ago. The idea was to say — under the thought experiment of innovation and our modern understanding of it, as well as endogenous growth, growth theory, and macro in general — if you think of macro the variable is A, the state of knowledge, and if we don’t improve it we stay the same. If we just had all the ideas we have now, things would keep breaking and we’d have investment because I have to fix the computer I’m on, your car will break down, your house will need the windows repaired and the roof redone eventually. You’re going to do investment just to keep things going, but we wouldn’t be getting better at stuff. There’s diminishing returns to capital investment. So we can’t just rely on savings and investment. We need to improve the ideas. We didn’t get faster at transportation because of more wagons. We needed something much better than wagons.

What you can do as a thought experiment is say, “Imagine we just stopped innovating.” We would replace what breaks and stay where we are. You can use that insight to create an overall calculation of the social returns to R&D under some assumptions that you can then play with, that reveals an average return to that investment. I’ll show you the very simple baseline and then you can try to generalize it to confront a lot of other forces that you might think are important to deal with beyond the baseline. Then you could also think about how it relates to micro evidence, or other kinds of macro evidence.

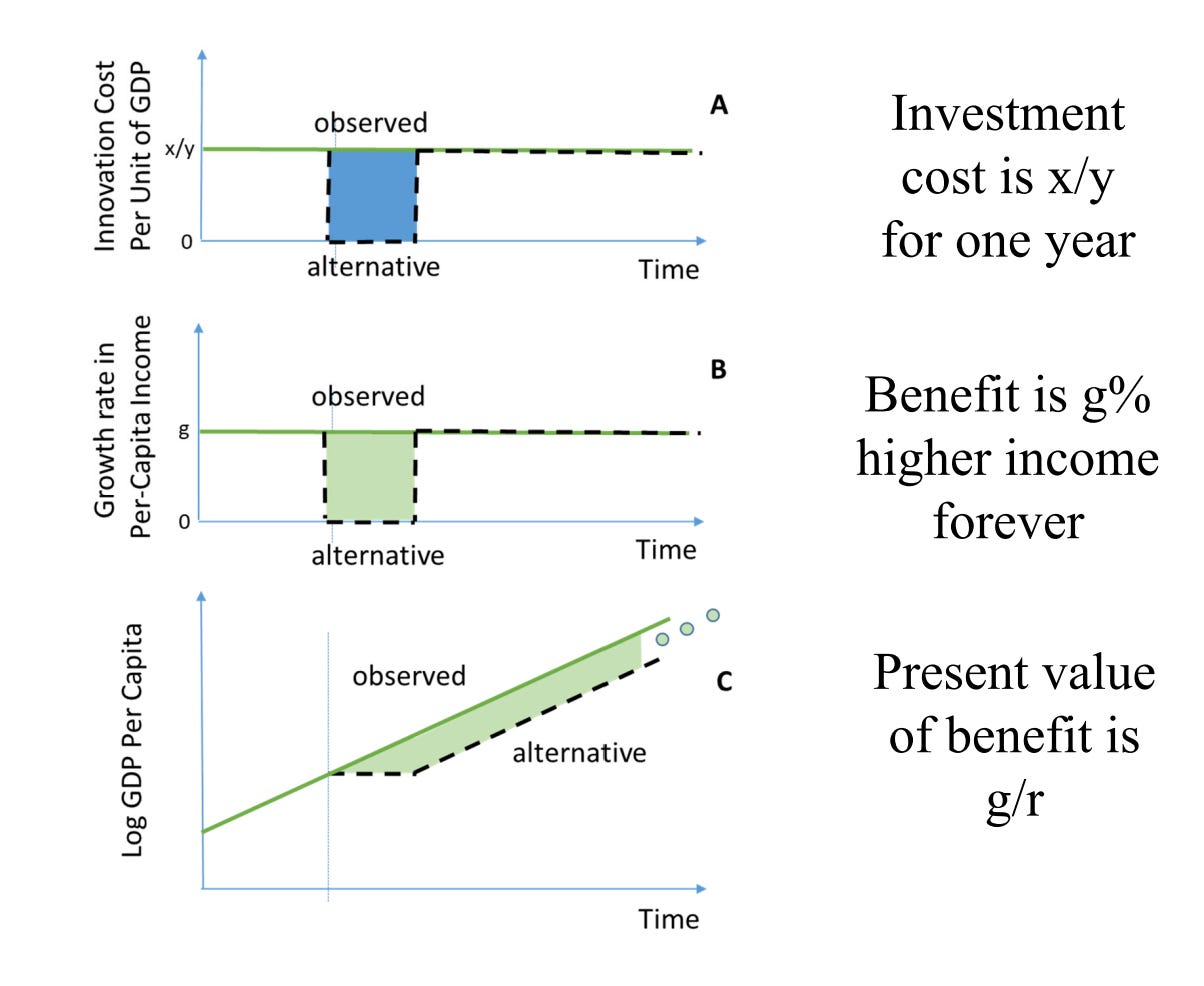

Here’s the thought experiment. It’s got non-rivalry, temporal spillovers, imitation — it’s netting it all together.

Look at the upper row. Imagine you’re investing, on the green line, a certain amount of your total GDP into R&D — or innovative activity, however you want to measure that. R&D is 2-3% of GDP in most advanced economies. You’re following the green line. Then for one year, you’re going to go on to the black line, where everyone stops. We stop the course. You guys go work somewhere else for a while. The labs — we just put some sheets over the equipment. A year later, we come back, we pull the sheets off the equipment, and keep going on exactly the same projects that we were doing before. We just had a year-long delay. We don’t change the pathway of discovery. It’s the same projects and the same intertemporal set of projects. They’ll inspire the same things, but we just delay it a year. We save a bunch of money by not having to do it for a year. That’s what we invest in innovation. That’s the top line.

The next line is what would happen to growth in a simple model. If we don’t advance the state of knowledge, we stay at the same standard of living. So we’d be growing at — most advanced economies 2% per year — and then we wouldn’t grow for a year in the middle row, and then we just grow again on exactly the same path. To put this in income per capita terms, in the lowest row, you’d be growing at a log scale like 2% per year going up, and then for a year you wouldn’t grow at all. You wouldn’t get rich or poor, you just didn’t advance ideas, and then you would advance ideas again at the same rate as before.

What’s the cost and what’s the benefit?

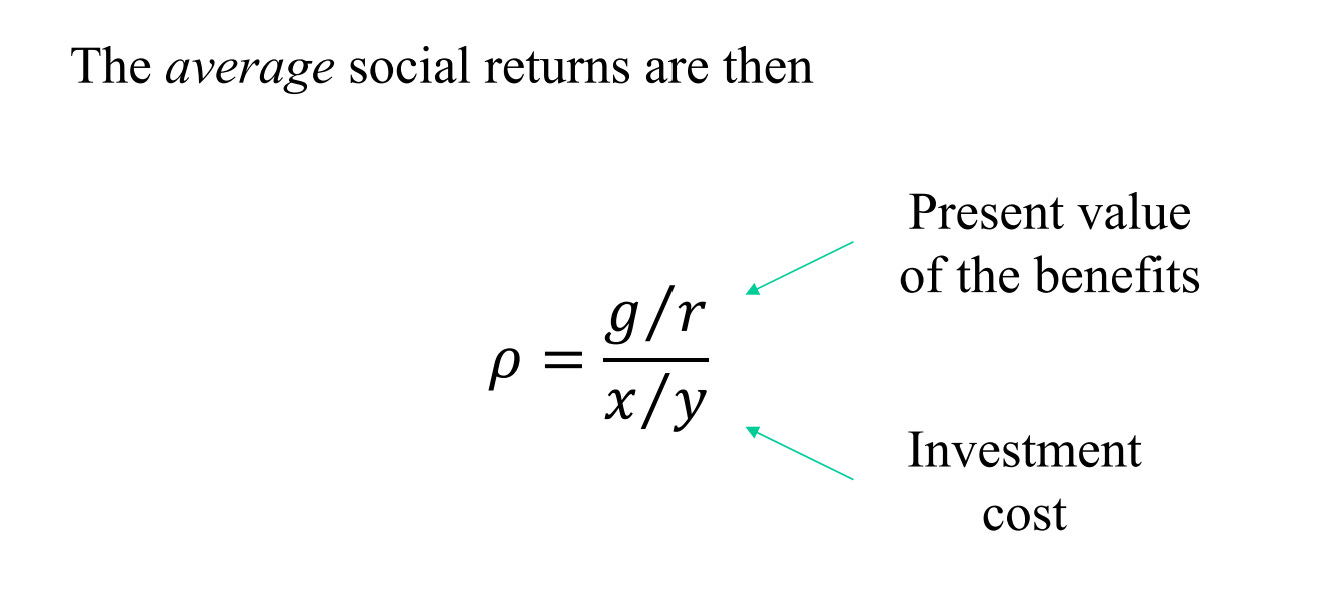

f you invest 2-3% of your GDP in a given year, you would be 2% richer forever, because you would grow that year and you’d keep it, you don’t forget the ideas, they don’t depreciate, we still know algebra. So the value of that is this green wedge in the lowest row. In every future period, you’re going to be 2% richer if you invested in those ideas than if you didn’t. What’s the present value of being g% richer in every period? Its present value is g/r, where r is some discount rate. In other words, you invest a share x/y of your resources. That’s the cost in R&D for a year, and you get to be g/r in present value terms. That’s the thought experiment. There’s maybe a lot of imitation, there’s business stealing, all sorts of things are going on in a given year of R&D. Firms are destroying each other, some are winning, some are losing. Many drugs fail, some win, but on net, we get 1.8-2% richer per year. That gives us the net of all of that effort.

The present value of the benefits is g/r. The cost of investment is x/y from a share of resources. That’s the social benefit cost ratio. Now think about this intuitively. x/y is 2-3% of GDP, but you’re 2% richer next year — and the year after forever. That’s an amazing thing, because if you push up the level of ideas quite a bit today, given our R&D investment, and you get that benefit forever.

What do you get from that calculation?

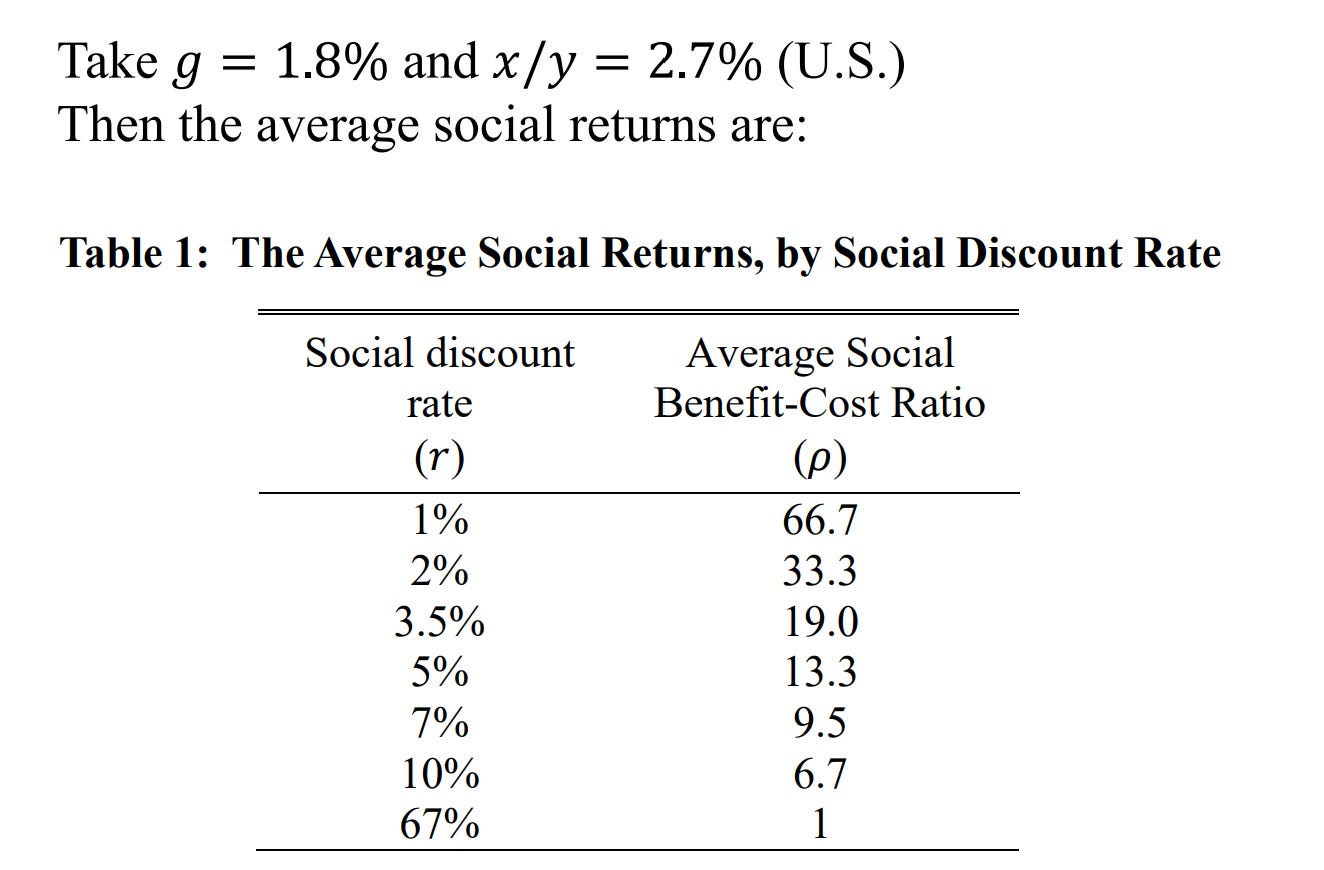

g is something like 1.8%, 2% more accurately in the US. x/y is 2.7%. You can pick your discount rate, but I’m going to take a 5% discount rate. Look at that table below, you’ll see it says 13.3. That means, for every dollar we spend on R&D, we get $13 back in present value, which is incredibly high. It’s like a machine: you put in a dollar, you get all this money back. The logic that’s driving that is because you push up the level, and people generations from now are going to be smarter, because there’s Riemannian geometry. They’re able to figure out how to use it. The ideas don’t go away. You push things up and it stays there. And it turns out we don’t spend that much.

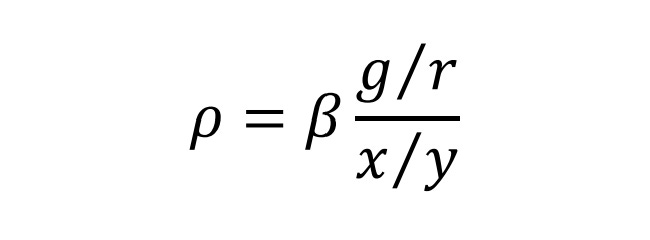

Maybe you think R&D formally measured is more than 2.7%. Maybe there’s a lot of innovation happening other ways and it’s badly measured. So this whole paper is about making this baseline calculation and then trying to kill it by making all sorts of different assumptions. You could put an adjustment factor I call β in front of that ratio.

Why would my $13 per dollar be too high?

It might be because there’s lags: I invest now but I don’t get the growth right now, I get it for science sometime in the future.

Maybe I have to embody the ideas in physical capital — they have to go into a smartphone, I have to spend on the smartphone.

Maybe other sources of innovation are out there — not just people doing formal R&D.

On the other hand, there’s a bunch of reasons that that baseline might be too low.

In macro we think that inflation is actually lower than we say because there’s a new goods bias if you follow that literature, so actually growth is higher than 1.8% in real terms. Maybe it’s more like 2.3% or 2.5%. That makes the returns to R&D even higher.

We don’t actually value health directly in GDP. A lot of research is trying to make you healthier and live longer, not to make higher income per capita based out of productivity on the job.

International spillovers. If the US does R&D, other countries can learn as well. So we’re a net exporter of ideas — the gain in standards of living can be far beyond your own borders.

You can balance these forces out. The conclusion is that it’s really hard to get the number of the benefit to be small compared to the cost, however you try to attack this. We actually said that on the very conservative end, you get $4-5 out per dollar. So this is a method where you’re trying to calculate the average return.

Where would that leave us? This is one version of the social returns. There’s many papers about the social returns to R&D doing different approaches, including a couple of very new ones. One of which, Fieldhouse and Mertens, is really about public investment in R&D alone and science, and it’s showing incredibly high returns. Not every paper agrees, but what you tend to see across a wide range of methods is repeatedly calculating very high social rates of return to idea creation. The paper I just showed you gives you some of that logic, because you push things up in a meaningful way that you benefit from in a future stream from your investments today.

In light of that, it seems like there are really high social returns. A lot of these papers are going to show higher returns on the margin. If we did another $1 billion of basic science, it’s going to be really valuable for society. So that means that both we’re going to have a bunch of institutions that are going to try to push on this, but also probably that they are currently way underfunded compared to their social benefit. Even conditional on their funding, do we have a good idea about the best way to design a science grant, or the patent system, or to run a university, or to create incentives for human capital like the tenure system, or how we give credit? All of these things are very open.

The questions in the bigger picture are:

What are those policies?

What are the right institutional structures?

How should we design and fund these various systems?

There’s a big policy question. Then there are a lot of questions about understanding idea creation that are really interesting from a personal and a private sector perspective:

Who captures value?

How do you capture value from data?

Where do you get excludability?

Who gets credit?

How does uncertainty affect our ability to produce and exchange ideas? There are some really interesting breakdowns in the market for ideas because of uncertainty between buyers and sellers. There are a lot of strategic interactions in markets in the production of ideas.

Then there are really big questions:

Where do big ideas come from?

Who produces them?

How do they come up?

What is one scholar doing versus another, versus an inventor, versus an entrepreneur?

Does someone have a better process? What is that process?

Are there better incentives? What are those incentive systems?

What is the role of AI in all this? It’s coming at us very fast. Is it going to fundamentally change how we do things?

Let me close, trying to motivate you a little:

I tried to get across how important this subject is. The social returns to R&D are very high, because if you can make this system more efficient, the returns for society are vast.

It’s not an area where we’re just studying it because it’s curious and markets get it right. It needs interventions, and there are so many kinds. It’s a very complicated space, and there’s so much to be learned at a very micro level, to more industry sector levels, to macro levels, about how to do that well. That’s going to require great research.

This is a growing area with amazing data. When I started out doing this long ago, there was patent data. There was no data on papers and scientists. There was no real good data on entrepreneurs. There wasn’t really data on funders and who’s funding what. We didn’t have the full text of anything. Between the data sets that have emerged, and the tools that have emerged in parallel, both our classic econometric tools and compute that we have, but also now all these AI tools, in addition to our causal identification and structural tools, it is a vast opportunity, and there’s theoretical opportunities as well.

I have gotten to the point where every single data set I touch, I’m like, “I could spend the next 15 years on this data set,” and then I have to go over to something else. There’s so much data. Another way to say that is, our scarcity right now in the economics of innovation is not opportunity or data. It’s people. We need more people on that mountain figuring it out. I think there are great opportunities to find your own niche that is of great interest to the whole community on the mountain.

I hope this course, in addition to giving a taste of what people are doing at the frontier, and some of the core questions, can inspire you to realize how much great work there is to be done. I hope we can attract you into this research community.